What Documents Do You Need to Sell Your House for Cash in Pennsylvania

Selling your house for cash is faster than a traditional sale. You skip the bank loans and waiting periods. But you still need paperwork to make it legal and official.

Many homeowners worry about documents. They think selling for cash means tons of confusing forms. The good news? A cash sale actually needs fewer documents than a regular sale. You do not need mortgage approval papers or bank statements.

This guide shows you exactly what documents you need to sell your house for cash in Pennsylvania. We will cover what you must provide, what the buyer brings, and what to do if you are missing something.

Understanding how selling a house for cash works starts with knowing your paperwork. When you know what to gather ahead of time, the whole process moves smoothly. You can close in as little as seven days when everything is ready.

Let's break down each document you need and why it matters.

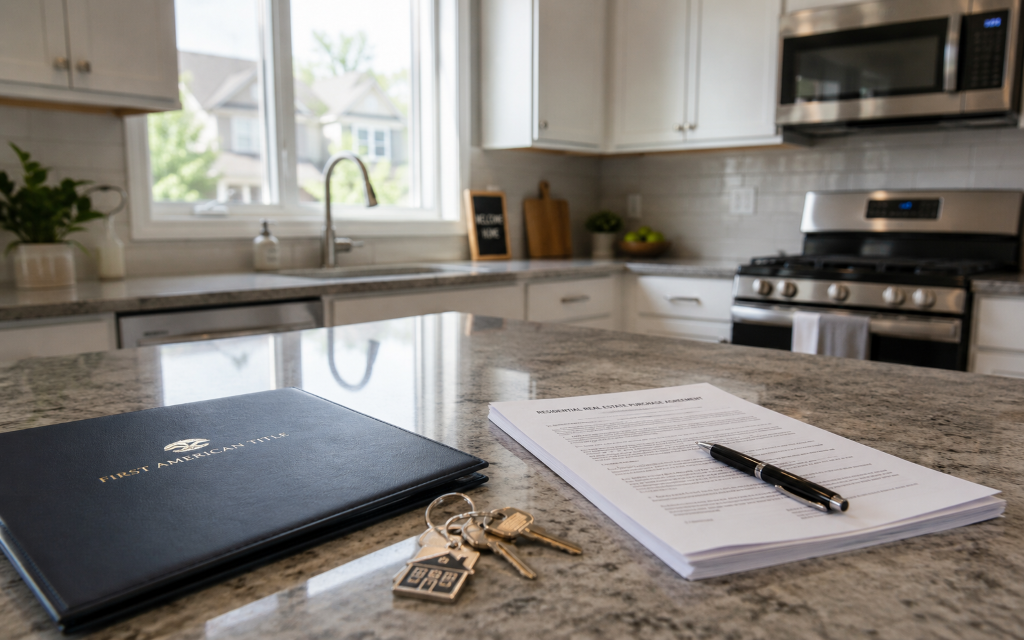

Required Documents for Every Cash Home Sale

Every as-is home sale in Pennsylvania needs certain basic documents. These prove you own the house and can legally sell it. Think of these as the must-have items on your checklist.

First, you need your property deed. This paper shows that you are the legal owner. If you paid off your mortgage, you should have received the deed in the mail. If you still owe money on the house, your mortgage company holds it. Don't worry if you cannot find your deed. We will explain how to get a copy later.

Second, gather your photo ID. A driver's license or state ID works perfectly. The title company needs to verify your identity before the sale. This protects everyone from fraud.

Third, collect any home inspection reports you have. These are not always required, but they help. If you had an inspection done in the past few years, include it. Cash buyers like Pezon Properties often buy houses as-is, so old reports still provide useful information.

Fourth, find your property tax records. These show your current tax status. The title company checks to make sure all taxes are paid. If you owe back taxes, the buyer usually pays them at closing and subtracts that amount from your offer.

Fifth, get your utility bills for the past month. This includes electric, gas, water, and sewer. These prove the utilities are in your name. They also help the buyer understand monthly costs.

Sixth, locate your homeowner's insurance policy. You need to show proof of coverage up to the closing date. After closing, you can cancel the policy and get a refund for unused months.

Lastly, bring any HOA documents you have. Homeowner association papers include rules, fees, and contact information. Not every neighborhood has an HOA, so skip this if it does not apply to you.

These seven items form the core of your document checklist. Most homeowners already have these papers somewhere in their house. Start looking for them as soon as you decide to sell.

Documents the Cash Buyer Will Provide

Good news: the cash buyer handles most of the paperwork. When you work with a legitimate cash buying company, they prepare the legal documents. This saves you time and stress.

The buyer provides the purchase agreement first. This contract lists the sale price, closing date, and terms. Read it carefully before signing. The agreement protects both you and the buyer. It puts everything in writing so there are no surprises.

Companies like Pezon Properties make this agreement simple and clear. They explain each section in plain English. You should understand every part before you sign. Never feel rushed to sign something you do not fully understand.

Next, the buyer arranges for title work. They hire a title company to research your property's history. The title company creates a title report. This report shows any liens, claims, or issues with the property.

The title company also prepares the settlement statement. This document breaks down all the numbers. It shows the sale price, any deductions, and your final payout. You see exactly how much money you will receive at closing.

The buyer also provides proof of funds. This shows they actually have the cash to buy your house. A bank letter or account statement works as proof. This step is important because it demonstrates that the sale will not fall through due to financing issues.

Your cash buyer also orders a title insurance policy,. This protects the new owner if any title issues arise later. The buyer pays for this insurance, not you.

Finally, the buyer brings certified funds to closing. This means a cashier's check or a wire transfer. You walk away from closing with payment in hand. No waiting 30 days for a bank to approve a loan.

Working with a professional company means you do not chase down paperwork. They handle the heavy lifting. Your job is to provide your basic documents and show up to closing.

What Happens If You Cannot Find Certain Paperwork

Missing documents? Don't panic. This happens all the time. Most paperwork can be replaced or worked around.

Let's start with the deed. If you lost your property deed, the county recorder's office has a copy. In Pennsylvania, visit your county's recorder of deeds office. You can request a certified copy for a small fee, usually around $10 to $20. Some counties let you order online. This process takes just a few days.

Cannot find tax records? No problem. Property tax information is public. Your county tax assessor's office has all your records. You can print them from their website or request copies by phone. Cash buyers can also look these up themselves.

Lost your home inspection report? That is okay too. Many cash buyers do not require inspections. They buy houses in any condition. If the buyer wants an inspection, they will arrange and pay for a new one.

Missing HOA documents? Contact your homeowner's association directly. They keep copies of all rules and financial statements. They can send you new copies, often by email. If you do not know your HOA contact, check your property tax bill. It sometimes lists the HOA information.

What about utility bills? If you cannot find recent bills, log in to your online accounts. Most utility companies let you download statements. Or call the company and request copies. They can email or mail them to you within days.

Property survey missing? A survey shows your property boundaries. It is helpful but not always required for a cash sale. The title company can sometimes find an old survey in its records. If needed, the buyer may order a new survey.

Here is the key point: be honest about missing documents. Tell your cash buyer right away. They work with this situation constantly. They know how to get replacements or move forward without them.

Pezon Properties and other reputable buyers help you track down missing paperwork. They have relationships with title companies and county offices. They can often get documents faster than you can on your own.

The title company also helps fill in gaps. They have access to public records and historical documents. They piece together what is needed for a legal sale.

In rare cases, you might need to sign an affidavit. This is a sworn statement explaining why you cannot provide a document. For example, if you inherited a house and never had certain documents, an affidavit can serve as a substitute.

The bottom line? Missing documents slow things down a little, but they rarely stop a cash sale. Cash buyers expect some missing paperwork. They build extra time into their process to handle these issues.

Start gathering what you have now. Make a list of what you are missing. Then work with your buyer to fill in the blanks. Together, you can get everything needed for a smooth closing.

Remember, selling for cash is still faster than a traditional sale, even when documents are missing. A regular sale requires mountains of financial paperwork from the buyer. Cash sales skip all that. You are still weeks ahead of a conventional closing.

Frequently Asked Questions

Can I sell my house for cash if I still have a mortgage?

Yes, you can absolutely sell your house for cash

even with an existing mortgage. The title company handles the payoff at closing. They contact your mortgage lender and get the exact payoff amount. This amount gets subtracted from your sale price. You receive the difference after the mortgage is paid off. Many homeowners sell this way when they need to move quickly or cannot afford their current payments. The cash buyer coordinates with your lender to make sure everything is paid correctly. You do not have to contact your mortgage company yourself.

How long does it take to gather all the necessary documents?

Most homeowners can gather basic documents in one to three days. Your deed, ID, and tax records are usually easy to find. If you are organized and keep files, you might have everything in a few hours. If you need to request copies from the county or utility companies, add three to five business days. Missing documents rarely delay a cash sale by more than a week. Cash buyers like Pezon Properties work around your timeline. They can start the process while you gather paperwork. The key is to start looking as soon as you decide to sell.

Do I need a lawyer to sell my house for cash in Pennsylvania?

Pennsylvania does not require you to hire a lawyer for a cash home sale. However, many sellers choose to have one review the purchase agreement. A real estate attorney costs around $500 to $1,000 in Pennsylvania. They make sure you understand all the terms and that the contract protects your interests. The title company handles most legal aspects of the closing. They are licensed professionals who ensure that everything complies with state law. If you feel comfortable with the purchase agreement and trust your buyer, a lawyer is optional. If anything seems confusing or concerning, hiring an attorney gives you peace of mind.

About the author

Mathew Pezon

Mathew Pezon is the founder and CEO of Pezon Properties, a cash home buying company located in Lehigh Valley, Pennsylvania. With several years of experience in the real estate industry, Mathew has become a specialist in helping homeowners sell their properties quickly and efficiently. He takes pride in providing a hassle-free, transparent, and fair home buying experience to his clients. Mathew is also an active member of his local community and is passionate about giving back. Through his company, he has contributed to various charities and causes.