Cash Closing Explained: What Actually Happens on Closing Day

Selling your house for cash can feel like stepping into unknown territory. What happens on closing day? Will you really get paid? Where do you go? Who else will be there?

The good news is that cash closings are much simpler than traditional home sales. There are fewer steps, fewer people involved, and less waiting around. When you understand how selling a house for cash works, you will feel more confident about the whole process.

This guide walks you through exactly what happens on closing day when you sell to a cash buyer. You will learn where you go, what papers you sign, and when the money hits your account. By the end, closing day will feel like just another appointment instead of a scary unknown.

How Cash Closings Are Different From Traditional Closings

Traditional home sales involve many people and many steps. A typical closing includes the buyer, the seller, two real estate agents, a lender, and a title company representative. Everyone has to coordinate schedules. The buyer's mortgage has to be approved at the last minute. Sometimes closings get delayed because the bank needs more paperwork.

Cash closings cut out most of these complications. There is no mortgage lender, as the buyer already has the funds. This means no last-minute loan denials. No waiting for bank approvals. No extra inspections demanded by mortgage companies.

At a cash closing, you typically meet with just the title company representative. Some cash buyers, like Pezon Properties in Allentown, PA, handle everything through the title company, so you do not even need to meet the buyer in person. This keeps things simple and comfortable.

The timeline is also much faster. Traditional closings usually happen 30 to 45 days after you accept an offer. Cash closings can happen in as little as seven days. Some sellers close in two weeks. You get to pick a date that works for your schedule.

Another big difference is the paperwork. Traditional closings involve stacks of documents. You sign your name dozens of times. Cash closings have fewer papers because there are no mortgage documents to review. You still sign important papers like the deed transfer, but the whole process takes 30 minutes instead of two hours.

Cash buyers

also purchase homes "as is" in most cases. This means no repairs before closing. No renegotiating after inspections. What you agree to at the start is what happens at closing. This removes a lot of stress and uncertainty from the process.

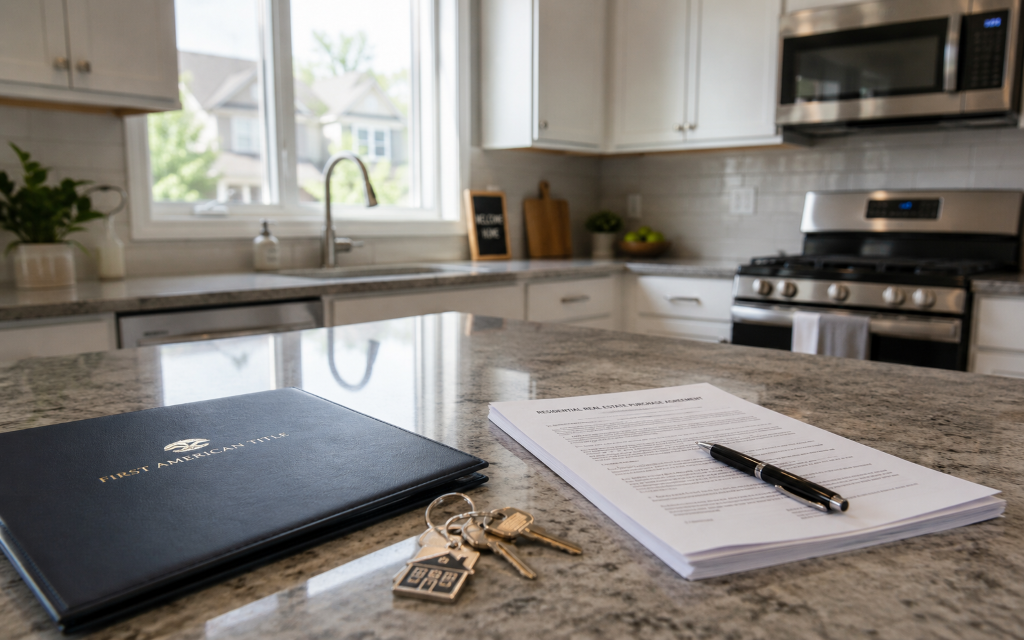

Where the Closing Takes Place and Who Attends

Most cash closings happen at a title company office. The title company is a neutral third party. They make sure all the legal paperwork is correct. They also hold the money until everything is signed properly.

When you sell to a cash home buyer, they usually choose a title company they trust. You can ask to use your own title company. Most buyers are flexible about this detail.

The title company office is usually a simple meeting room with a conference table. You will sit down with a closer or settlement agent. This person works for the title company. Their job is to walk you through each document and answer your questions.

In many cash sales, the buyer does not attend the closing. They sign their papers ahead of time or at a separate appointment. This is actually nice for sellers. You do not have to sit across from the buyer and feel awkward. You just handle your paperwork and leave.

Some title companies offer mobile closings. A notary comes to your home, your workplace, or a coffee shop. You sign the papers wherever is most convenient for you. This service makes closing day even easier, especially if you have young kids or a busy work schedule.

Pezon Properties works with experienced title companies in the Allentown area. They handle all the scheduling. You just show up, sign the papers, and move on with your day.

You should bring a government-issued ID to closing. A driver's license or passport works. You should also bring the keys to your house, garage door openers, and any alarm codes. Some title companies ask for proof of address, but this varies by company.

The whole appointment typically takes 30 to 45 minutes. Sometimes less. You are not sitting there for hours like you might with a traditional closing.

When and How You Receive Your Money

This is the part everyone cares about most. When do you actually get paid?

With cash closings, you usually receive your money the same day you sign the papers. Sometimes it takes one business day. The title company processes everything and sends the funds to your bank account.

You can choose how you want to receive payment. Most people prefer a wire transfer directly to their bank account. Wire transfers are fast and secure. The money shows up within hours of closing.

Some sellers prefer a cashier's check. If you choose this option, you get a check at the closing table. You can deposit it at your bank right away. Cashier's checks are guaranteed funds, so they clear quickly.

Here is how the money flow works. The cash buyer sends their money to the title company before closing day. The title company holds it in an escrow account. This is a safe, neutral account. After you sign all the papers, the title company releases the money to you.

Before you get paid, the title company subtracts certain costs from the sale price. These include property taxes you owe, homeowner association fees, or liens on your property. If you owe money on a mortgage, the title company pays that off first. You get whatever money is left over.

The title company gives you a settlement statement before closing. This document shows exactly how much money you will receive. It lists every deduction and every cost. Review this carefully. If something looks wrong, ask questions before you sign anything.

Most cash buyers cover many of the closing costs themselves. This means you keep more of the sale price. Traditional sales often require the seller to pay thousands in fees and commissions. Cash sales usually have lower fees and no real estate commissions.

Within 24 hours of closing, check your bank account to confirm the money arrived. If you chose a wire transfer and do not see the funds, call the title company right away.

What Happens to Your Mortgage and Other Liens

If you still owe money on your house, the title company handles the payoff. You do not need to contact your mortgage company yourself. The title company does this for you.

Here is the process. Before closing, the title company orders a payoff statement from your lender. This statement shows exactly how much you owe, including any interest up to the closing date. The title company uses part of the sale proceeds to pay off this loan on closing day.

After the mortgage is paid, your lender releases the lien on your property. A lien is a legal claim against your house. Once released, the buyer gets a clean title with no claims against the property.

Other liens get handled the same way. If you have a home equity loan, that gets paid off at closing. If you owe back taxes, those get paid. Suppose there is a mechanics lien from unpaid contractor work, that gets satisfied. All of this happens automatically through the title company.

Sometimes sellers owe more on their mortgage than the house is worth. This is called being underwater or upside down. In these cases, a traditional sale might not work because you cannot pay off the loan with the proceeds of the sale. Some cash buyers can help negotiate a short sale with your lender, though this takes more time and approval.

The title company runs a title search before closing. This search finds all liens and claims against your property. Nothing should surprise you on closing day because the title company identifies these issues beforehand.

If your house has a second mortgage or HELOC (home equity line of credit), both loans must be paid off before you receive any money. The first mortgage gets paid first, then the second mortgage, then any other liens. You receive whatever is left.

Property taxes also get handled at closing. If you owe taxes for the current year, the title company pays them from your proceeds. If you already paid taxes for the whole year but are selling partway through, you might get a credit for the unused portion.

Homeowner association fees work similarly. If you owe HOA dues, they get paid at closing. The title company makes sure everything is current before transferring the deed.

When working with Pezon Properties, you can understand all these costs upfront. They can estimate your net proceeds before you agree to anything. This way, you know exactly what to expect on closing day.

Frequently Asked Questions

Can I change my mind after signing the closing papers?

Once you sign the deed and the closing is complete, you cannot back out of the sale. The house legally belongs to the buyer at that point. This is why it is important to review all documents carefully before signing. If you have doubts, ask the title company to explain anything you do not understand. You can also bring a lawyer or trusted advisor to closing if you want extra support. Most cash buyers, including Pezon Properties, work hard to ensure you feel comfortable and informed throughout the process.

What if I need to stay in the house for a few days after closing?

Some cash buyers offer rent-back arrangements. This means you sell the house but

continue living there for a short time while you pay rent to the new owner. Not every buyer offers this option, so ask early in the process if you need extra time. The rent amount is usually reasonable and is outlined in the purchase agreement. Rent-back periods typically last one to four weeks. This flexibility helps sellers who need time to move or find a new place. Make sure any rent-back agreement is in writing and signed by both parties before closing day.

Do I need a lawyer at a cash closing?

In Pennsylvania, you do not legally need a lawyer at closing, but you can bring one if it makes you feel more comfortable. The title company handles most legal details and makes sure all documents are correct. Many sellers complete cash closings without an attorney and have no problems. If your situation is complicated, such as going through a divorce or dealing with an estate sale, a lawyer might be helpful. The lawyer can review documents and protect your interests. Most cash buyers are fine with you bringing legal representation to closing.

About the author

Mathew Pezon

Mathew Pezon is the founder and CEO of Pezon Properties, a cash home buying company located in Lehigh Valley, Pennsylvania. With several years of experience in the real estate industry, Mathew has become a specialist in helping homeowners sell their properties quickly and efficiently. He takes pride in providing a hassle-free, transparent, and fair home buying experience to his clients. Mathew is also an active member of his local community and is passionate about giving back. Through his company, he has contributed to various charities and causes.